How the pandemic has worsened the medical debt crisis

GUEST BLOG AUTHOR: Emily Taylor, Boston College, BA, Class of 2022 (Summer 2021 Health Care Campaigns Intern)

Like many other Americans, I’m starting to picture the end of the past year and half shaped by COVID-19. With new cases decreasing and vaccination rates increasing, it looks like we may have cleared the worst months of the pandemic. But there are still other challenges that linger.

From January 2020 to March 2021, an additional 2.5 million Americans fell into medical debt, adding over $2 billion to the total medical debt burdening families today. Now, as we emerge from the quarantine, return to work in-person, and attempt normalcy once more, medical debt will haunt many families in the months and years ahead.

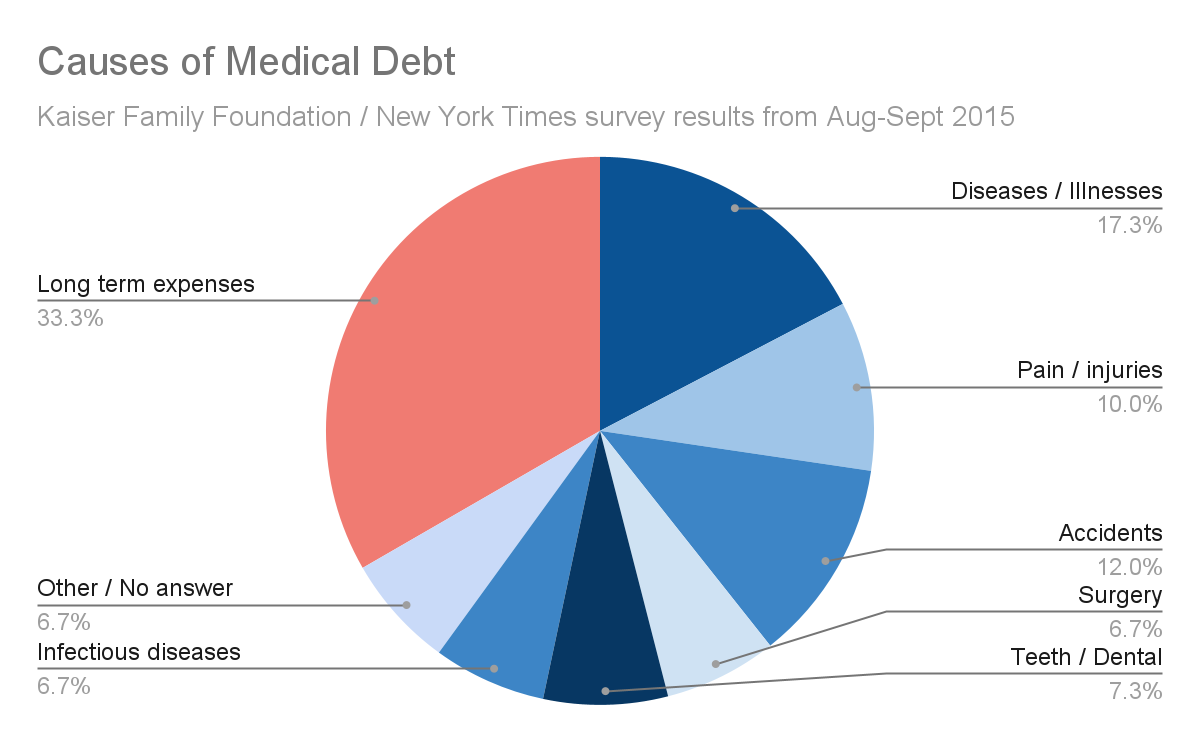

Medical debt is any sum owed to a health care provider or collection agency for any medical services or products. A common misconception is that medical debt primarily affects uninsured patients. However 62 percent of those with medical debt had insurance coverage when receiving care. Another common assumption is that medical debt arises from ongoing treatment for chronic illnesses and conditions, but surprisingly two-thirds of all medical debt is caused by short term or one-time events. Unlike other incurred debt more likely controlled by consumer decisions and choices, medical debt arises from uncontrollable and unpredictable circumstances, such as emergencies, accidents, and illness. The chart below explains the many causes of medical debt. All of the blue slices represent the short-term or one-time causes of medical debt and the red (about ⅓ of debt) shows all possible causes of medical debt arising from long-term expenses.

Source of data: Kaiser Family Foundation

Two unique factors combined to put 2.5 million more Americans into medical debt during the first 18 months of the spread of the COVID virus: increased need for expensive treatment for the millions who contracted COVID and significant job lay-offs which resulted both in loss of income as well as the loss of employer-sponsored health insurance.

Treatment for COVID-19 is expensive. For an uninsured patient aged 51 to 60 hospitalized with COVID, care costs an average of $45,683. Even with insurance, the cost of COVID treatment is still tens of thousands of dollars. Given the median bank account balance for Americans is $5,300, it is no surprise families can’t afford their treatment and incur medical debt.

The bills don’t stop once you leave the hospital either. Andréa Ceresa told NBC News that although she’s paid over $20,000 towards her bill, she still owes $133,000 from her hospitalization after contracting COVID-19 in November 2020. In addition to this debt, she’s incurring more bills in follow-up care for the long-term effects of the virus — more bills she cannot pay off, especially now that she can’t return to work due to health complications.

Mounting bills from COVID treatment and long-term effects have been exacerbated by the loss of income and employer-sponsored insurance. Over 22 million jobs were lost during just four months of the pandemic (January-April 2020) with unemployment rates reaching the highest rate since 1948 when records were first kept (14.8% at the height of the pandemic in April 2020). While it is hard to determine, estimates show anywhere from 3 million to 7 million people lost employer sponsored insurance during the pandemic. However, over 2 million people enrolled in health insurance during the 2021 Marketplace special open enrollment periods, partially offsetting the loss of employer sponsored health insurance. But the combined effect of job loss and lack of insurance exposed many families to high out-of-pocket medical bills, whether for COVID treatment or other medical needs, that they simply could not pay off.

As more people grapple with unpaid medical bills, hospitals are ramping up their debt collection actions, using the courts and contracted debt collection agencies to track down payments. Some of the largest health systems in the country sued for more than $72 million during the pandemic. Alarmingly, 65 percent were not-for-profit hospitals, which are required by law to provide charity care to low income patients. Instead, they left the most vulnerable families at risk of financial harm as they struggle to emerge from the pandemic. Court judgments can result in liens on property, garnishment of wages, and court-ordered payment plans. These actions can be financially devastating to families struggling to pay other bills and might still be looking for work or recovering from COVID or other health issues. Medical debt is tied to homelessness or bankruptcy. While some of the larger hospitals continue to collect on unpaid medical bills, most hospitals had stopped collection actions at least temporarily or otherwise used federal relief aid to help pay for uninsured patients.

As Americans return to health and to offices, they will struggle to pay off the debt racked up during the pandemic. State and federal governments are considering how to help Americans handle the financial burdens they could not expect or control. Consumer advocates are urging leaders to implement medical debt solutions that help keep families in their homes and food on the table while people work to pay off their unavoidable health bills.

Photo credit: Set of American cash money and medical facial masks – Karolina Grabowska from Pexels (Canva.com)

Senior Director, Health Care Campaigns, U.S. PIRG Education Fund

Patricia directs the health care campaign work for U.S. PIRG and provides support to our state offices for state-based health initiatives. Her prior roles include senior policy advisor at NJ Health Care Quality Institute, associate state director at AARP New Jersey and consumer advocate at NJPIRG. She was appointed to the Ground Ambulance and Patient Billing Advisory Committee in 2022 and works with patient advocates across the U.S. Patricia enjoys walking along the Potomac River and sharing her love of books with friends and family around the world.